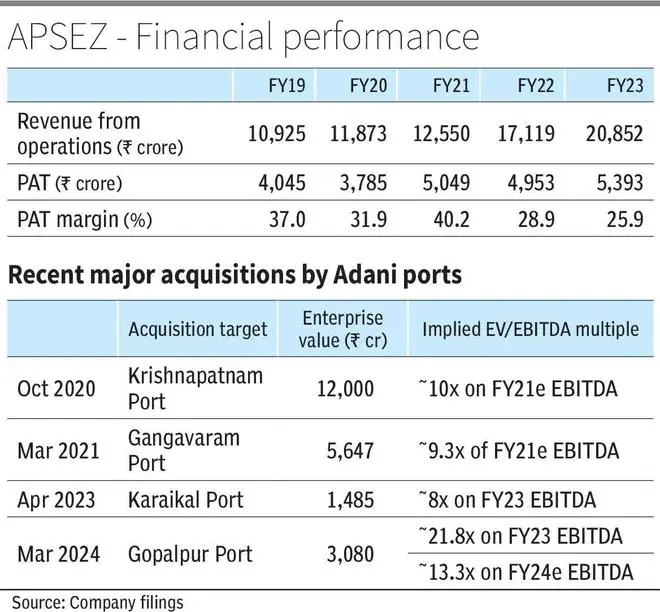

Adani Ports and Special Economic Zone Ltd (APSEZ), India’s largest ports and logistics company, will purchase a 95% stake in Gopalpur Port Limited (GPL), which includes a 56% stake from Shapoorji Pallonji (SP) Group and 39% in Orissa Stevedores Limited (OSL). The equity consideration for the 95% stake is ₹1,349 crore, with an enterprise value of ₹3,080 crore in an all-cash deal. The transaction is expected to be completed by Q1 FY25.

In line with APSEZ’s long-term strategic goal

APSEZ currently has 14 strategically located ports and terminals (seven each on the West and East coast). It has a total capacity of ~607 Million Metric Tonnes (MMT) (West ~355 MMT and East ~252MMT). Gopalpur Port, located on the East coast of Odisha with a capacity of 20 MMT, will be the seventh Indian port acquired by the Adani Group through the inorganic route since 2014. Others include Dhamra (50MMT), Kattupalli (25), Krishnapatnam (75), Gangavaram (64), and Karaikal (22) on the East Coast (236 out of the current East capacity of 252MMT has been through inorganic acquisition) and Dighi (8) on the West. As a result of the strategy to expand its presence on the East coast, the share of East in domestic cargo volumes handled by APSEZ has increased from nil in FY14 to 43% in 1HFY24. This has enabled the Company to make significant strides in capturing market share of domestic cargo volumes, which has risen from ~11.6% in FY14 to an estimated ~26.2% in FY24.

Financials and valuation

GPL handled 7.4 MMT of cargo and generated operational revenue of ₹373 crore in FY23. It is estimated to handle about 11.3 MMT cargo (YoY growth - 52%), earn a revenue of ₹520 crore (YoY growth of 39 per cent), and achieve EBITDA of ₹232 cr (YoY growth of 65 per cent) in FY24. It handles a diverse mix of dry bulk cargo, including iron ore, coal, limestone, and alumina. The Government of Odisha awarded a 30-year concession to GPL in 2006, providing two extensions of 10 years each. The port is well connected to its hinterland through the national Highway NH16, and a dedicated railway line connects it with the Chennai-Howrah main line. It recently signed up with Petronet LNG Ltd to set up a greenfield liquefied natural gas (LNG) regasification terminal, adding predictable long-term cash flows for the port.

APSEZ expects higher operational efficiencies and infra-debottlenecking in FY25. The deal implies an EV/EBITDA multiple of ~13x on estimated FY24 numbers, a ~60% premium to its recent acquisition of Karaikal port in April 2023 at 8x EV/EBITDA on FY23 numbers. The company is quite optimistic about the future earnings potential of Gopalpur’s location since it will allow unprecedented access to the mining hubs of Odisha and neighbouring states, thereby expanding its hinterland logistics footprint. APSEZ reported revenue ₹20,852 crore in FY23. GPL is expected to add ~2% to its overall revenue in FY24. It is currently trading at an implied EV/EBITDA multiple of 21x/18x on FY24/FY25 EBITDA (Bloomberg consensus). Given the Company’s track record of turning around ports in the past and the earnings potential of Gopalpur port, the current deal is expected to prove value accretive for investors.

![]() Comments

Comments